(Bloomberg) — Big Oil has a powerful ally in the White House, but the first quarter of Donald Trump’s presidency was a real test for companies’ plans. The rest of the year could be even tougher.

Most Read from Bloomberg

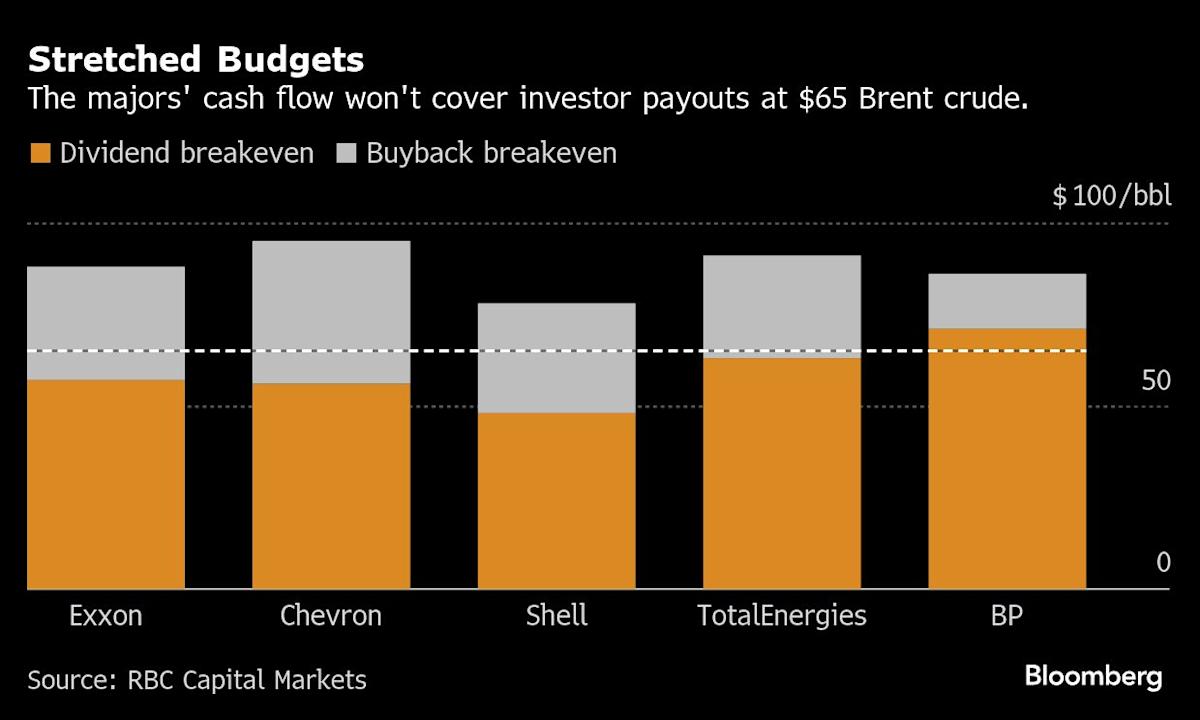

The US leader’s desire for lower crude prices and his disruption of the global economy with trade tariffs is stressing the industry’s finances, calling into question both shareholder returns and drilling plans.

Of the five global oil majors that report earnings next week, BP Plc is first in line and the most exposed to recent volatility. Even before Trump’s trade war, the company’s debt was rising and it had told investors to expect a reduction in quarterly share buybacks of as much as $1 billion.

The struggling UK company is not a total outlier. Chevron Corp.’s investor payouts are under pressure, with analysts expecting the oil major to trim its buyback 6% after the price of a barrel of crude plunged into the $60s. All of the majors, including Exxon Mobil Corp., Shell Plc and TotalEnergies SE could be tempted to slow spending on new projects as long as Trump is roiling markets.

“For the trade war at the moment, it probably makes it a bit harder to make any investment decisions,” said TD Cowen Managing Director of Energy Equity Research Jason Gabelman. “It wouldn’t be shocking if you see some of these project decisions get pushed out.”

Big Oil’s unease was on clear display in Oklahoma City last week, when Occidental Petroleum Corp. Chief Executive Officer Vicki Hollub told a room full energy, technology and government officials that for all its passion for oil and gas, the Trump administration lacks a holistic energy plan.

Already, companies are changing their investment plans for 2025 to bolster their balance sheets. To maintain its share buyback amid declining cash flow, Italy’s Eni SpA said it had taken action to reduce spending. Var Energi ASA, Norway’s third biggest oil and gas company, said it could slow down some project developments.

Analysts expect other companies to prioritize their share buybacks and dividends over capital expenditure.

Generous payouts have become crucial to Big Oil’s appeal to investors. The commodities rally that followed the Covid-19 pandemic and Russia’s invasion of Ukraine led to record profits and bumper returns, an opportunity to tempt back shareholders who had fled the sector. Four of the five Big Oil stocks reached record highs between 2022 and 2024.

The majors faced a reality check toward the end of 2024, when crude plunged and profit margins from making fuel and chemicals faltered. The situation worsened this year, when initial optimism about Trump’s “drill baby, drill” agenda turned into gloom as his trade war — combined with unexpected supply hikes from the Organization of the Petroleum Exporting Countries and its allies — sent prices tumbling to four-year lows.

The five supermajors — Exxon, Chevron, Shell, TotalEnergies and BP — are expected to report combined profits of $22.5 billion for the first quarter, 11% higher than the previous three months due to slightly higher oil prices, but about half the levels seen in 2022, according to data compiled by Bloomberg.

Shell is seen having a strong quarter compared with its peers, after giving guidance that oil production would be higher than planned and crude trading posted a good performance. Chevron’s buybacks and dividend are expected to exceed its free cash flow by more than $4 billion, indicating it will need to increase debt, reduce spending or dip into cash reserves to fund its payouts.

A key industry bellwether — US shale producers — is already indicating the direction of travel for the majors. Known for responding quickly to market dynamics, operators in the oil-rich US Permian Basin, where Chevron and Exxon hold prominent positions, are cutting spending to compensate for falling cash flow.

Shale operator Matador Resources Co. said it will drop one of its drilling rigs due to plunging crude prices, slicing $100 million from its planned capital expenditures for the year. Fellow Permian player Diamondback Energy Inc., is actively reviewing its operating plan for the year. BP’s Denver-based shale unit, which was running nine drilling rigs in US onshore basins from January to March, has dropped one Permian rig, according to energy data provider Enverus.

Lower crude prices aren’t the only challenge. Globe-spanning oil giants’ intercontinental supply chains could be vulnerable to Trump’s tariffs in unexpected ways, said Fernando Valle, managing director at Hedgeye Risk Management, LLC. The impact on each company will depend on the strength of their balance sheet, asset inventory and where the bulk of their business operates, he said.

For example, BP’s US onshore oil and gas business sources its steel and aluminum from within the country, so won’t see any impact from tariffs, Chief Executive Officer Murray Auchincloss said at the company’s annual general meeting in London on April 17. Its offshore business, however, depends on imports of specialty steel from overseas, he said.

“Our team in Washington is very busy with all the changes that are occurring,” Auchincloss said. “The impact on the business so far is not material.”

Ultimately, decision-making will depend on the length and severity of oil’s slump and Trump’s tariffs, with significant operational changes taking much longer than a single quarter.

“Big Oils typically don’t turn on a dime,” said HSBC’s Head of European Oil and Gas Research Kim Fustier.

(Updates with BP earnings preview in third paragraph.)

Most Read from Bloomberg Businessweek

©2025 Bloomberg L.P.