(Bloomberg) — US government bonds rallied Wednesday after Federal Reserve officials kept interest rates steady, as expected, while trimming their economic growth and boosting their inflation forecasts based on increased uncertainty.

Most Read from Bloomberg

Treasury yields fell from near session highs, erasing increases of four to five basis points and declining, most by several basis points. The two-year note’s, more sensitive than longer-dated tenors to changes in expectations for US monetary policy, was around 3.97% after peaking above 4.08%.

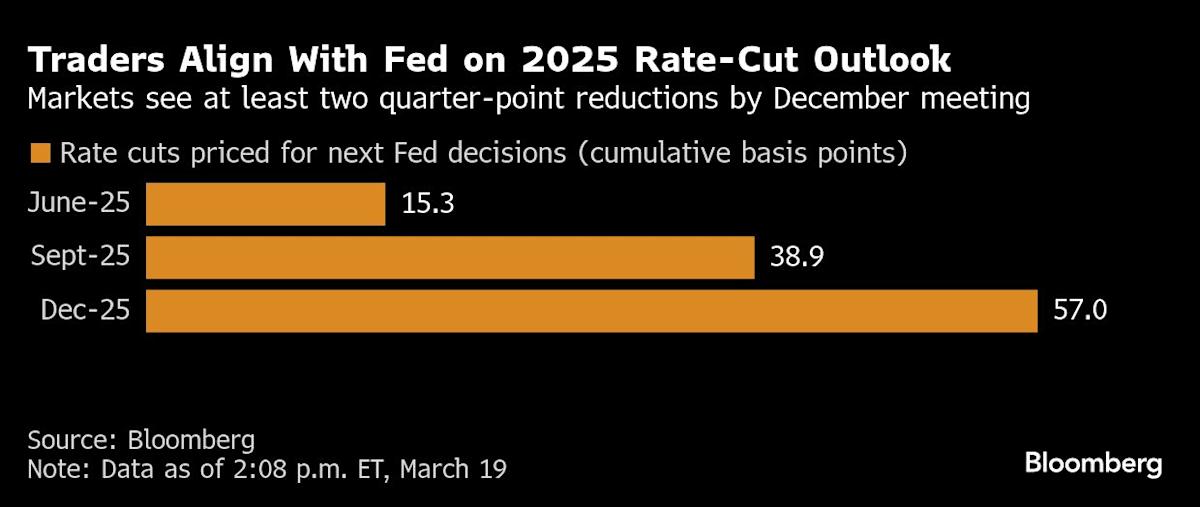

Policymakers two-day March meeting kept their target for the US overnight lending rate at 4.25%-4.5%, and their median forecast for where it will end the year remained at 3.875%, anticipating two quarter-point cuts this year. They paused cutting rates in January with inflation still exceeding the 2% long-term target and the job market remaining healthy.

Traders continued to price in a similar outcome, with the first cut predicted as soon as July. Last week the market-implied prediction was closer to three quarter-point cuts. Several major Wall Street banks have predicted no further rate cuts by the Fed this year, however, so the stable median forecast bolstered the camp looking for cuts.

“It’s neither dovish or hawkish, it’s the Fed calling a timeout until its May meeting and doing it’s best to a find a middle ground amidst a wide distribution of outcomes,” said George Catrambone, head of fixed income, DWS Americas. “The fact investors saw hawkishness and dovishness in the statement means they’ve done their job for the moment.”

The central bank also said it would slow the pace of decline in its holdings of Treasuries beginning next month. That will support the Treasury market by the limiting the supply of notes and bonds sold to private investors.

Fed Chair Jerome Powell — who recently said “the economy’s fine” and didn’t need help from the Fed — said in the news conference after the meeting that while “uncertainty today is unusually elevated,” the central bank remained in no hurry to change policy.

Powell said sticky inflation was “partly in response to tariffs, and there may be a delay in further progress in the course of this year,” but also that policymakers’ base case is that “inflationary will be transitory.”

While the Fed median signaled two cuts for this year, there was a narrowing of the distribution among officials. While nine policymakers penciled in two cuts, compared to 10 in December, now eight officials only see one or no cuts, compared with four in December. Two policymakers say there will be three cuts and none see more than that, compared with five saying three or more cuts in December.