(Bloomberg) — The Federal Reserve’s decision to cut the pace of its balance-sheet unwind is leading some Wall Street strategists — including those at Barclays and Bank of America — to push out their expectations for how long the central bank’s runoff will go on.

Most Read from Bloomberg

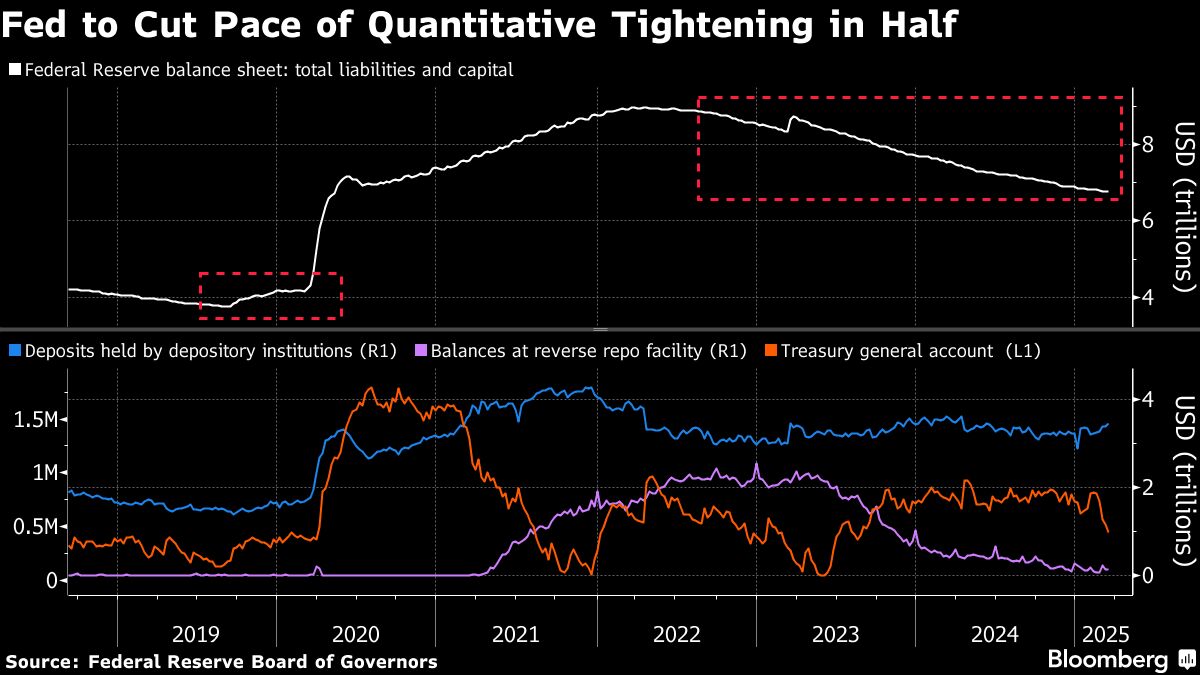

Officials, who left interest rates unchanged on Wednesday, said that starting April 1 they’ll lower the cap on the amount of Treasuries allowed to mature without being reinvested to $5 billion from $25 billion. The Fed will leave the cap on mortgage-backed securities unchanged at $35 billion.

The central bank has been winding down its holdings since June 2022 — a process known as quantitative tightening, or QT — by gradually increasing the amount of Treasuries and mortgage bonds it allows to run off without being reinvested.

Barclays Plc now sees that program ending in June 2026 instead of September of this year, while Bank of America Corp. pushed out its expectation for the end of the runoff to December of this year, from September previously.

There is not a clear consensus on Wall Street and some strategists, like the ones at Deutsche Bank, say that the change this week is unlikely to change the timing of the end of quantitative tightening.

The divergent expectations underscore the uncertainty around how short-term funding markets will respond to the current impasse around the debt ceiling.

Lawmakers are attempting to strike a deal on the debt ceiling, the statutory limit for outstanding Treasury debt. The US hit that limit in January. The longer it takes Congress to either suspend or lift the limit, the more cash will make its way back into the financial system. That has the potential to artificially boost reserves — currently $3.46 trillion — which would make it hard to read the signs in the money markets that would indicate the proper timing for ending QT.

It’s those money-market signals that will dictate just how much more the Fed will be able to shrink its $6.8 trillion portfolio of assets before worrisome cracks start to appear, as they did in 2019 ahead of an acute funding squeeze.

In a somewhat worrying sign, Chair Jerome Powell said that officials had seen some signs of increased tightness in money markets, a key deliberation for the timing and path of quantitative tightening, even as reserves remain abundant in the financial system. He also said “if you’re cutting the pace of QT, roughly, in half then the runway is probably doubled.”

What the Strategists Say

Bank of America (Mark Cabana, Katie Craig, March 19 report)

-

Now sees the Fed stopping QT at the end of December 2025 from September previously, and expects the central bank to wait until after the debt limit resolution and rebuild of the Treasury General Account to reevaluate balance-sheet policy

-

Longer QT path implies an additional $180 billion in SOMA reduction versus BofA’s prior expectation of a paused announced at the March meeting. This will result in a slightly faster pace of drain in the overnight reverse repo facility once the debt limit is resolved, as well as a greater reserve drain

-

Expect RRP usage to fall to zero by September 2025 and reserves to be about $3 trillion at the end of QT, or 9.75% of GDP, and sees the Fed starting to buy T-bills in 1Q 2026 at a pace of $10 billion per month

Barclays (Joseph Abate, March 20 report)

-

Now estimates the Fed could end QT in June 2026 from September 2025, noting that if the central bank keeps its new pace through next year the level of reserves will shrink to about $2.7 trillion, or about 11% of bank assets

-

Once the Fed has reached “this efficient level, how long can it remain there before it will need to resume secondary market Treasury purchases to maintain this equilibrium,” something that likely depends on the size of the precautionary cushion it wants to leave in the market

-

It’s unclear where the “signs” of tightness are since the fed funds rate has been pinned at IORB-7bp since 2022 and the reserve demand elasticity measure remains near zero, While triparty repo rates have climbed by 3 basis points since last year, they’re still well below IORB

Deutsche Bank (Matthew Raskin, Steven Zeng, Brian Lu, March 19 report)

-

Continue to anticipate Fed’s runoff will end in 1Q 2026

-

Adjustment in Treasury reinvestment cap will result in $120 billion less balance sheet runoff over the next six weeks, which is on the “modest end of the measures the FOMC could take to mitigate risks around the debt limit”

-

Powell’s mention that the Committee has seen “some signs of increased tightness in money markets” is stronger language that may signal reserves are nearing ample than has featured in recent communications. “All else equal, this should have made the Committee more, not less, worried about debt limit dynamics”

JPMorgan Chase (Jay Barry and others, March 19 report)

-

Now expect QT to run at the current pace through 1Q 2026, citing Powell’s comment about doubling the runway by cutting the runoff in half, as well as Dallas Fed President Lorie Logan’s comments on balance sheet last month

-

There’s still a risk there may be stresses in the funding markets when the Treasury General Account is rebuilt after the resolution of the debt ceiling, though the slowdown in pace of QT will likely “dampen the effect of these stresses”

-

See Fed’s balance sheet declining to about $6.6 trillion by end-2025, with overnight reverse repo facility balances falling to about $50 billion and reserve balances to $3 trillion during that time

RBC Capital Markets (Blake Gwinn, Izaac Brook, March 19 report)

-

“The destination remains the same (as of yet unknown, but the same as it was yesterday). They are just going to approach that destination a bit more slowly”

-

The additional $20 billion per month of Treasuries the Fed will now have to buy will be done as “add-ons” at auctions, which means there will be more on-the-run collateral available in the central bank’s daily securities lending operations, preventing repo specialness in these securities

-

$20 billion less bill supply per month could drive some marginal richening in T-bills, though if the terminal size of the balance sheet isn’t changing, “the delayed issuance will eventually come, and outstanding bill supply will end up at the same spot. It will just take a slightly different path to get there”

TD Securities (Gennadiy Goldberg and others, March 19 report)

-

Expect Fed to discontinue QT altogether at the September FOMC meeting since the policy will become “inconsistent with the Fed’s likely restart of rate cuts” in the second half of 2025

-

Fed’s decision is a function of “significant uncertainty” as the debt ceiling impasse persists

-

Risk is that with QT running at a very slow pace, Fed could decide to keep the runoff in place for longer

Wells Fargo (Angelo Manolatos, March 19 report)

-

Now sees QT potentially ending in 3Q, likely September instead of June, as Powell believes cutting the speed of the runoff in half can double the remaining life of the balance—sheet unwind

-

Still questions about Treasury reinvestments once QT ends. Strategists assume once the the runoff concludes, the majority of MBS principal will be reinvested in T-bills, in addition to reserve management purchases once the central bank starts growing the asset side of its balance sheet in 1Q 2026

-

Strategists remain bullish on swap spreads since net Treasury issuance to the private sector will decline by $20 billion a month. Other tailwinds include potential regulatory relief and improving financing needs in 2025

Wrightson ICAP (Lou Crandall, March 20 report)

-

While Powell said the QT slowdown has no implications at all for the ultimate size of the balance sheet, “things may very well work out that way but, as the FOMC’s change of heart this week demonstrates, the Fed’s policy stance – with respect to the balance sheet as well as rates – will always adapt to changing circumstances”

-

Most immediate consequence of the slowdown is the Treasury will have to trim the supply of bills a little more until its debt limit constraints are resolved, which could amount to $60 billion in both 2Q and 3Q

-

That could result in an additional $5 billion cut in both the six- and eight-week bill auction sizes, though timing is uncertain since assumptions after the April tax season are “very approximate”

Most Read from Bloomberg Businessweek

©2025 Bloomberg L.P.