(Bloomberg) — Treasuries climbed as the fallout from President Donald Trump’s tariffs convulsed markets for another day.

Most Read from Bloomberg

Two-year yields fell notes fell to their lowest since September 2022 earlier in the session and benchmark 10-year yields slumped as much as 17 basis points to 3.95%. But the rally faded somewhat after a solid US jobs and comments from Fed Chair Jerome Powell suggested that the central bank is focused on the impact of tariffs on inflation dashed expectations for immediate rate cuts.

Still, money markets have priced in nearly four quarter-point rate reductions this year, up from just three cuts before the levies were announced Wednesday.

Listen to the Here’s Why podcast on Apple, Spotify or anywhere you listen

“Everything today is being driven by the expectation that the economy is going to take a major hit,” said Jan Nevruzi, an interest-rate strategist at TD Securities.

Earlier in the session, China announced it would impose a 34% tariff on all imports from the US, raising the specter of a global trade war. Later, Powell said the economic impact of new tariffs is likely to be significantly larger than expected.

It was the central bank chief’s first public appearance since March 19, when policymakers opted to hold rates steady, as expected. Then, the Fed lowered median projections for GDP and lifted those for inflation. Still, Powell said after the meeting that policymakers’ base case was that a tariff-induced inflation bump would be transitory.

On Friday, Trump urged the Fed to cut interest rates, one day after he said he welcomed the slide in 10-year yields. Treasury Secretary Scott Bessent has said repeatedly that lower Treasury yields are a priority for the administration.

“Trump will tell them to feel the market and eventually they will cut — not in May, though,” said Neil Dutta, head of US economic research at Renaissance Macro Research. Powell “is focused on inflation expectations even as financial conditions have tightened. That’s hawkish, all else equal.”

Risk Aversion

The ongoing reaction across markets has been stark. The S&P 500 saw its worst two-day plunge since March 2020 in a rout that has shed about $5 trillion in value, with the gauge down 6% on Friday. The Nasdaq 100 entered a bear market.

Markets have priced in a roughly 50% probability of a quarter-point rate reduction at the next Fed meeting in May. Some traders are even betting on an emergency rate cut before the May 6-7 meeting, with open interest in the April fed funds futures soaring.

Many of the moves persisted even after March employment data released Friday showed that 228,000 nonfarm jobs were created, exceeding the 140,000 median forecast of economists in a Bloomberg survey. January and February job gains were revised lower, though, and the unemployment rate ticked up to 4.2%.

What Bloomberg strategists say…

“A lot of this bond market rally will have to be reversed in the next couple of months. And with no relief from discount rates implied by Treasury yields, equities will suffer even more as a consequence. This is stagflation with inflation as the binding constraint.”

—Edward Harrison, “The Everything Risk” Newsletter, Washington

“The bond market is seeming to keep its focus on the tariff news,” said Zachary Griffiths, head of investment-grade and macroeconomic strategy at CreditSights.

Global Pain

European bonds have been swept up in the bond rally, anticipating a hit to growth from the 20% US tariff. Germany’s 10-year yield, the regional benchmark, has plunged this week, erasing the surge unleashed by the nation’s increased spending plans in March.

Traders also expect the European Central Bank to lower rates more sharply, with three quarter-point reductions fully priced in for this year and a chance of a fourth. The Bank of England also is seen easing 74 basis points.

The global bond surge even saw sub-zero rates return in some corners. The bid yield on two-year Swiss government bonds turned negative for the first time since 2022.

The Swiss National Bank cut its key policy rate to 0.25% from 1.75% last year, and traders are betting on at least another quarter-point cut by the end of 2025, with some hedging for further easing. Bloomberg Economics estimates US tariffs could reduce US demand for Swiss goods goods by around 60%.

For Mark Dowding, chief investment officer at RBC BlueBay Asset Management, the repricing has already gone far enough. He doubts that both the Fed and ECB will be able to respond to tariffs with monetary easing, citing inflationary concerns in the US and an emphasis on fiscal support in Europe, and is instead looking for entry points to bet against bonds once markets settle.

“The rally in bond yields appears overdone,” he wrote in a note. “We think the Fed will do nothing for the foreseeable future, as long as there is not a large rise in unemployment.”

Treasuries have already rallied 3.8% this year, according to a Bloomberg gauge of US debt.

Inflation Balance

In the US, Fed officials have said that a resilient labor market and sticky inflation mean they can afford to stand pat, even as Trump’s tariffs sapped consumer and business confidence.

“This jobs report is going to create an absolute mess for the Fed response to economic risks,” said Guy LeBas, chief fixed income strategist for Janney Montgomery Scott. “The ‘best’ case for risk assets is that the data deteriorate quickly enough to generate a Fed response. The bad case for risk assets is that jobs muddle through in the face of warmer short-term inflation prints.”

Economists generally expect that tariffs will lift inflation and slow growth, keeping the Fed in wait-and-see mode. But the tariffs unveiled Wednesday were larger than anticipated, clouding the picture. While Morgan Stanley now expects no cuts this year, down from one previously, citing inflation risks, UBS Global Wealth Management see more easing this year.

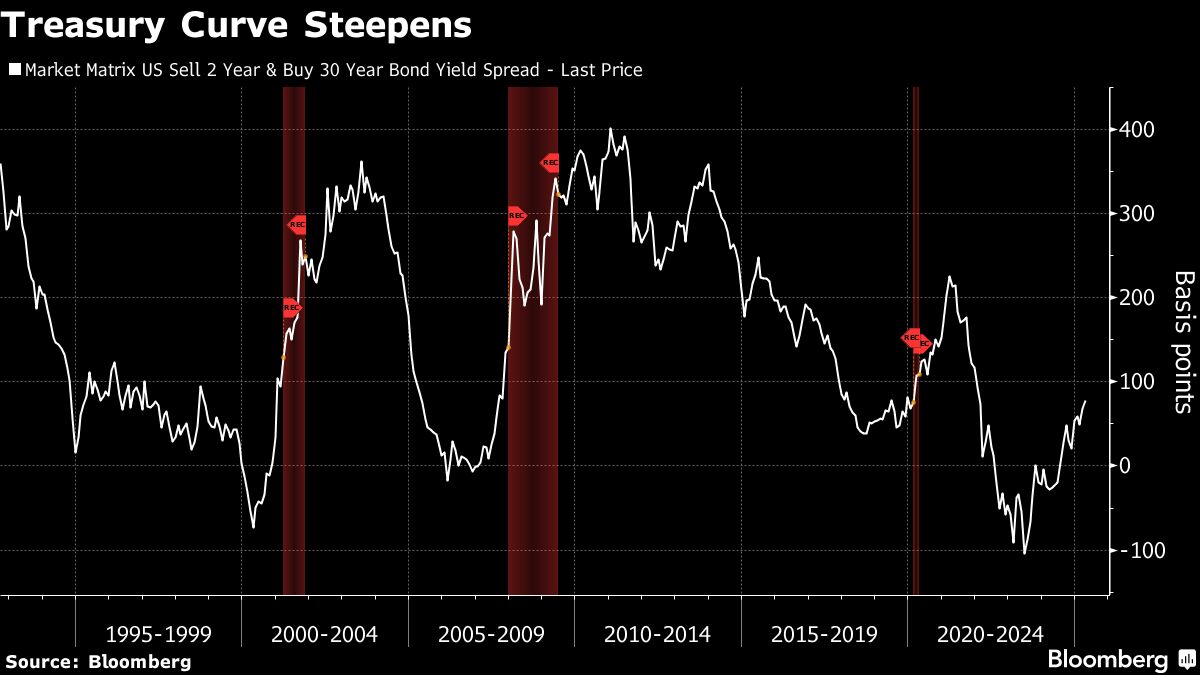

Vineer Bhansali, chief investment officer and founder of Longtail Alpha, said he’s buying two-year notes and selling 30-year bonds, a trade known as a curve steepener. It’s a bet that a slowing economy will force the Fed to lower interest rates, while elevated inflation would lead long-term bonds to underperform.

That growing wager is reflected in the market, with the yield difference between two-year and 30-year bonds widening.

“The distribution of possible outcomes has gotten flatter,” Bhansali said. “Anything can happen.”

Now that the US has announced broader tariffs, what are you doing with your investments? Tell us in the latest MLIV Pulse survey.

–With assistance from Alice Atkins, David Watkins, Greg Ritchie and Stephen Kirkland.

(Updates with late session pricing.)

Most Read from Bloomberg Businessweek

©2025 Bloomberg L.P.